All Categories

Featured

Table of Contents

[/image][=video]

[/video]

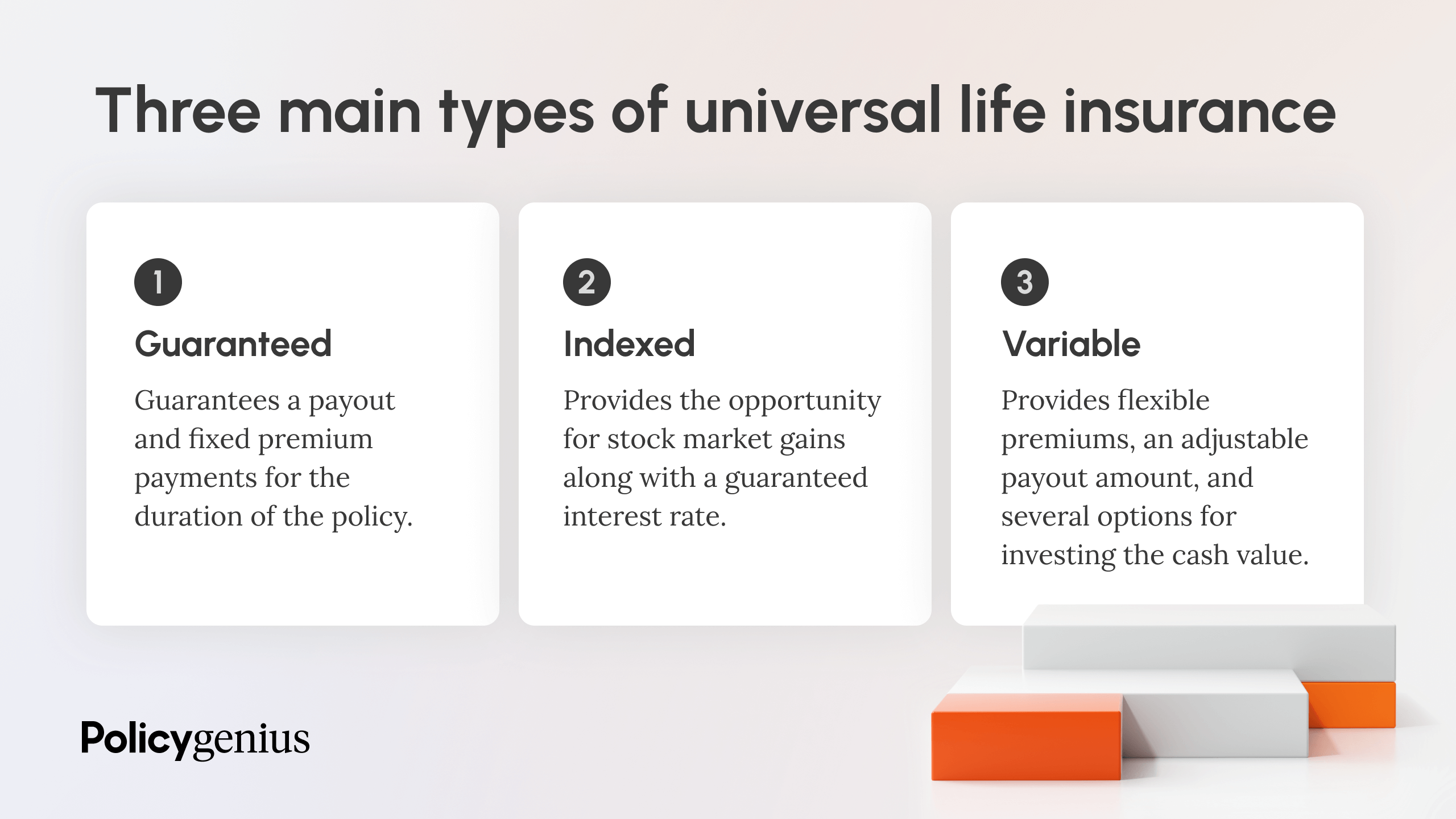

The plan obtains value according to a fixed schedule, and there are fewer costs than an IUL policy. Nevertheless, they do not come with the flexibility of adjusting premiums. features even more versatility than IUL insurance, implying that it is likewise much more difficult. A variable policy's cash money value might rely on the efficiency of specific supplies or various other securities, and your premium can likewise change.

An indexed global life insurance policy consists of a survivor benefit, as well as an element that is tied to a stock market index. The money value growth depends upon the efficiency of that index. These policies use higher prospective returns than other kinds of life insurance policy, along with higher dangers and extra fees.

A 401(k) has even more financial investment alternatives to pick from and might come with an employer match. On the other hand, an IUL includes a survivor benefit and an extra cash money value that the policyholder can borrow against. They likewise come with high premiums and charges, and unlike a 401(k), they can be canceled if the insured stops paying into them.

Nevertheless, these policies can be a lot more complex contrasted to other sorts of life insurance coverage, and they aren't necessarily right for each investor. Speaking with a knowledgeable life insurance policy representative or broker can help you make a decision if indexed global life insurance policy is a good fit for you. Investopedia does not supply tax obligation, financial investment, or financial services and suggestions.

What Is A Iul Investment

:max_bytes(150000):strip_icc()/Pros-and-cons-indexed-universal-life-insurance_final-1b83c0fd52154eb69edd47f99ab8927a.png)

IUL plan motorcyclists and personalization alternatives enable you to tailor the plan by increasing the death benefit, adding living benefits, or accessing cash worth earlier. Indexed Universal Life Insurance Policy (IUL Insurance Policy) is a long-term life insurance plan offering both a death advantage and a money value component. What sets it apart from other life insurance coverage plans is just how it takes care of the financial investment side of the cash money value.

It is very important to keep in mind that your cash is not directly invested in the stock exchange. You can take cash from your IUL anytime, but charges and give up fees may be associated with doing so. If you need to access the funds in your IUL policy, considering the advantages and disadvantages of a withdrawal or a loan is crucial.

Unlike straight investments in the stock market, your cash worth is not straight bought the underlying index. Rather, the insurance coverage firm makes use of economic instruments like alternatives to connect your cash worth development to the index's efficiency. One of the unique features of IUL is the cap and flooring prices.

Iul Training

Upon the policyholder's fatality, the beneficiaries obtain the survivor benefit, which is generally tax-free. The death benefit can be a fixed quantity or can include the money worth, depending upon the plan's structure. The cash worth in an IUL plan grows on a tax-deferred basis. This indicates you do not pay tax obligations on the after-tax capital gains as long as the money remains in the plan.

Constantly evaluate the plan's information and consult with an insurance policy professional to completely recognize the benefits, restrictions, and prices. An Indexed Universal Life insurance policy policy (IUL) provides an one-of-a-kind blend of features that can make it an appealing option for details individuals. Here are several of the crucial advantages:: Among the most enticing aspects of IUL is the potential for greater returns compared to various other types of long-term life insurance policy.

Taking out or taking a car loan from your policy may reduce its money value, death benefit, and have tax implications.: For those thinking about tradition preparation, IUL can be structured to give a tax-efficient means to pass wide range to the future generation. The fatality advantage can cover inheritance tax, and the cash worth can be an additional inheritance.

While Indexed Universal Life Insurance Policy (IUL) provides a range of advantages, it's vital to take into consideration the prospective drawbacks to make a notified decision. Here are a few of the key downsides: IUL policies are much more complex than standard term life insurance policy policies or whole life insurance policy policies. Recognizing how the cash money value is connected to a stock exchange index and the implications of cap and flooring rates can be testing for the ordinary customer.

Understanding Indexed Universal Life Insurance (Iul) ...

The premiums cover not just the cost of the insurance policy however also management charges and the investment component, making it a more expensive option. While the cash money value has the capacity for growth based upon a stock exchange index, that development is frequently covered. If the index does extremely well in a given year, your gains will be limited to the cap rate defined in your policy.

: Adding optional attributes or riders can boost the cost.: Just how the plan is structured, consisting of how the cash money value is assigned, can likewise affect the cost.: Different insurer have different rates models, so looking around is wise.: These are charges for taking care of the policy and are generally subtracted from the cash money value.

: The prices can be comparable, however IUL supplies a floor to help safeguard against market declines, which variable life insurance policy plans usually do not. It isn't simple to give a specific cost without a certain quote, as rates can vary dramatically in between insurance policy carriers and individual situations. It's critical to stabilize the significance of life insurance and the demand for added defense it provides with possibly greater premiums.

They can aid you recognize the costs and whether an IUL policy lines up with your economic goals and requirements. Whether Indexed Universal Life Insurance Coverage (IUL) is "worth it" is subjective and depends upon your monetary goals, risk tolerance, and long-lasting planning needs. Right here are some indicate take into consideration:: If you're seeking a lasting financial investment lorry that provides a death benefit, IUL can be a great alternative.

Secure your liked ones and save for retired life at the same time with Indexed Universal Life Insurance Policy.

Nationwide Iul Accumulator Review

Indexed Universal Life (IUL) insurance coverage is a sort of permanent life insurance policy policy that combines the functions of conventional global life insurance policy with the potential for cash value growth connected to the performance of a securities market index, such as the S&P 500. Like other kinds of irreversible life insurance policy, IUL supplies a death advantage that pays to the beneficiaries when the insured passes away.

Cash money worth build-up: A section of the costs repayments enters into a money worth account, which earns passion over time. This cash worth can be accessed or obtained against throughout the policyholder's life time. Indexing alternative: IUL plans provide the opportunity for cash money value development based on the performance of a stock market index.

As with all life insurance policy items, there is also a set of dangers that insurance policy holders should know prior to considering this type of policy: Market danger: Among the main risks connected with IUL is market risk. Because the cash money value growth is linked to the efficiency of a stock exchange index, if the index does badly, the cash worth may not grow as expected.

Indexed Universal Life Vs. Whole Life Insurance

Adequate liquidity: Policyholders ought to have a stable monetary situation and fit with the superior settlement requirements of the IUL policy. IUL permits flexible costs repayments within specific restrictions, however it's important to maintain the policy to ensure it accomplishes its designated objectives. Passion in life insurance policy protection: People that require life insurance policy coverage and a rate of interest in cash worth growth may discover IUL enticing.

Prospects for IUL should have the ability to comprehend the mechanics of the plan. IUL may not be the very best alternative for individuals with a high tolerance for market risk, those who focus on inexpensive financial investments, or those with even more prompt financial needs. Consulting with a qualified economic advisor who can provide customized support is essential prior to thinking about an IUL plan.

All registrants will receive a calendar invite and link to join the webinar using Zoom. Can not make it live? Register anyway and we'll send you a recording of the presentation the next day.

Iul Investment

Policy financings and withdrawals might create a negative tax outcome in the event of gap or policy surrender, and will lower both the abandonment value and death benefit. Clients should consult their tax consultant when considering taking a policy finance.

It must not be taken into consideration investment advice, nor does it constitute a suggestion that any person engage in (or avoid) a specific course of activity. Securian Financial Team, and its subsidiaries, have a monetary passion in the sale of their items. Minnesota Life Insurance Coverage Firm and Securian Life Insurance Policy Company are subsidiaries of Securian Financial Team, Inc.

In case you choose not to do so, you need to consider whether the item concerned appropriates for you. This website is not an agreement of insurance coverage. Please refer to the plan agreement for the specific conditions, specific details and exclusions. The policy discussed in this webpage are secured under the Plan Proprietors' Protection Plan which is provided by the Singapore Down Payment Insurance Coverage Firm (SDIC).

To find out more on the types of benefits that are covered under the scheme along with the limits of insurance coverage, where appropriate, please contact us or check out the Life insurance policy Organization, Singapore or SDIC websites () or (www.sdic.org.sg). This ad has not been evaluated by the Monetary Authority of Singapore.

{kind=link}

Latest Posts

A Quick Guide To Understanding Universal Life Insurance

Universal Indexed Life Insurance

Indexed Universal Life Insurance